A knowledge base for a fintech SaaS is not a generic help center with a security badge bolted on. The regulators reading your dispute-resolution article during an exam are not impressed by your SOC 2 logo. They want the article to be current, accurate, and consistent with what your product actually does. Most fintech KB writeups stop at SOC 2, audit logs, and encryption. Those are table stakes. The harder problem is what happens after the system is secure and the article is still wrong.

This guide covers what a fintech SaaS knowledge base needs that a generic SaaS knowledge base does not. It walks the regulatory frameworks that actually touch documentation, the eight technical requirements that show up on every fintech procurement checklist, the vendors that meet the bar, and the accuracy gap that SOC 2 does not close. It is written for compliance leads, heads of customer operations, and CTOs at Seed-to-Series-C fintechs whose Notion or Confluence wiki has outgrown its purpose and whose next compliance review will probably notice.

None of this is legal advice. Specific obligations depend on your charter, your jurisdiction, and your risk analysis. Always consult counsel and your compliance program before treating any vendor claim as the final answer.

Why fintech needs a different knowledge base

Most articles about fintech SaaS compliance focus on the security envelope. Encrypt at rest, encrypt in transit, sign a BAA for HIPAA-adjacent flows, gate access by role, log everything. That is correct as far as it goes. It is also incomplete.

The piece that fintech leaders learn during their first regulatory examination, not before it, is that the regulator reads the customer-facing documentation. The Consumer Financial Protection Bureau's Supervision and Examination Manual is explicit: examiners review policies, procedures, training materials, contracts, marketing collateral, and consumer-facing disclosures as part of the supervision process. The point of the review is to assess whether the firm's customer interactions match the regulation. If the help center article on how disputes are resolved diverges from the firm's actual practice, that gap is a finding. If the article references an out-of-date timeline, an out-of-date fee, or a product behavior that has since changed, that gap is a finding.

The same pattern applies under the Federal Financial Institutions Examination Council's IT Examination Handbook, under FCA Principle 7 in the UK ("communications fair, clear, and not misleading"), under BaFin's MaRisk guidance for outsourcing and operational documentation, and under GDPR Article 5's requirements for transparency in how personal data is processed. The exact language differs across jurisdictions. The structural posture is identical. Regulators look at what the customer sees. The knowledge base sits squarely in that field of view.

This is the part a generic SaaS knowledge base was not built for. Help center platforms have spent fifteen years optimizing for write velocity, search ranking, and team collaboration. They have not been built around the assumption that an external party with subpoena power will examine every article during a routine exam. Fintech changes that assumption.

Regulatory frameworks that touch documentation

The frameworks below all touch documentation in some way. The strength of the obligation varies. None of this is a substitute for a compliance program built with counsel, but knowing which framework demands what of a knowledge base is the starting point for any procurement conversation.

- KYC and AML. Bank Secrecy Act obligations require written policies, training materials, and customer-onboarding procedures. Regulators routinely request these documents during examinations. The customer-facing version of these procedures, the help center article that walks a customer through identity verification, must be consistent with the internal policy.

- PCI-DSS. The Payment Card Industry Data Security Standard governs environments where cardholder data is stored, processed, or transmitted. PCI-DSS itself is mostly about the production environment, but Requirement 12 requires documented security policies, and any KB article that describes how the firm handles card data needs to align with the policies under audit.

- PSD2. The EU's Payment Services Directive requires strong customer authentication and transparent disclosure of fees and processing timelines. Fintechs operating in EU markets need help center content that aligns with both the regulatory text and the SCA flow the customer experiences.

- GDPR. Article 5 requires lawful, fair, and transparent processing. Articles 12 through 14 specify what information must be provided to data subjects. The privacy notice and the help center articles that describe how data is handled both fall within the scope of these obligations.

- GLBA. The Gramm-Leach-Bliley Act requires US financial institutions to provide clear privacy notices and safeguards explanations. The customer-facing version of these notices lives in or links from the help center.

- CCPA and state privacy laws. California, Colorado, Virginia, and others require specific disclosures about data handling, retention, and consumer rights. The help center is the typical venue for these disclosures alongside the privacy policy.

- CFPB UDAAP. Unfair, deceptive, or abusive acts or practices. The CFPB has the authority to act on customer-facing communication that materially misleads. An outdated help center article describing fees or timelines is, in the wrong context, a UDAAP problem.

- FFIEC guidance. For fintechs partnered with chartered banks or operating with national bank charters, FFIEC guidance on third-party risk management and operational documentation typically expects firms to maintain accurate, current customer-facing materials and to evidence the review cadence.

The pattern across all of these is the same. The framework does not say "your knowledge base must do X." It says the firm must maintain accurate and current customer-facing communication. The knowledge base is the place that obligation lives.

The 8 fintech knowledge base requirements

These are the eight requirements that show up on almost every fintech procurement checklist. Items one through seven are the security and identity envelope. Item eight is the one most procurement checklists miss, and it is the one regulators care about most.

1. SOC 2 Type II and ISO 27001

SOC 2 Type II is the baseline. Type I attests that controls are designed correctly at a point in time. Type II attests that controls operated effectively over a review period of typically six to twelve months. For fintech vendor reviews, Type I is rarely accepted. ISO 27001 is increasingly expected on top of SOC 2 for fintechs operating in EU markets or selling into regulated banks. The vendor's most recent unredacted report should be available under NDA.

2. Audit logs of every edit and access

Regulators typically expect that the firm can produce a complete record of who changed what and when. For a knowledge base, that means tamper-resistant logs of every article edit, every permission change, every published version, and ideally every read on internal-only articles. Retention windows are jurisdiction-dependent. FFIEC guidance commonly cites seven years for log retention in banking contexts. Build for seven, settle for five at the minimum.

3. Content versioning with snapshot retention

The article that was live on the day of the exam is the artifact the regulator may ask for. The KB platform must capture immutable snapshots of every published version, with a way to retrieve "what did the article say on March 14, 2025" without ambiguity. KnowledgeOwl, Document360, and Zendesk Guide all offer versioning, but the retention windows and the snapshot guarantees vary. Verify the retention term before signing.

4. Role-based access for compliance reviewers

The compliance team needs read access to every article, including agent-only and internal articles. The legal team needs review-and-approve workflows on sensitive articles. The product team needs write access scoped to their surface area. The customer-facing version of the article must be locked from editing by anyone outside the approved publish workflow. RBAC at the section and article level is the floor, not the ceiling.

5. Encryption at rest and in transit

AES-256 at rest. TLS 1.2 or higher in transit. Search indexes and AI embedding caches must also be encrypted. Key management should be documented in the vendor's SOC 2 report. For fintechs in PCI-DSS scope, encryption-key rotation procedures should be visible during the review.

6. Data residency for EU and regional operations

Fintechs operating in the EU or processing EU residents' data need to evidence where the data lives. The major KB vendors offer regional hosting at the Enterprise tier. Zendesk's Data Center Location add-on covers US, EU, AU, and Japan. Document360 offers US, EU, and AU regions. Helpjuice runs on certified infrastructure but the regional options depend on the deployment. The procurement checklist should specify the region required and verify it is contractually pinned.

7. SSO and SCIM for identity governance

Finance teams use Okta, Azure AD, JumpCloud, or Google Workspace as the identity backbone. The KB must federate against the identity provider, and provisioning and deprovisioning should flow through SCIM so that a leaving employee loses access on the same day they leave. Every major vendor offers SSO at the Enterprise tier. SCIM is more variable. Verify both before signing.

8. Accuracy and freshness controls

This is the requirement no procurement checklist has historically included. SOC 2 Type II proves the system was secure. Audit logs prove who changed the article. Versioning proves what the article said on a given date. None of that proves the article was right. The accuracy gap is what regulators actually see during an exam, and we cover it in its own section below.

Vendors that meet the fintech bar

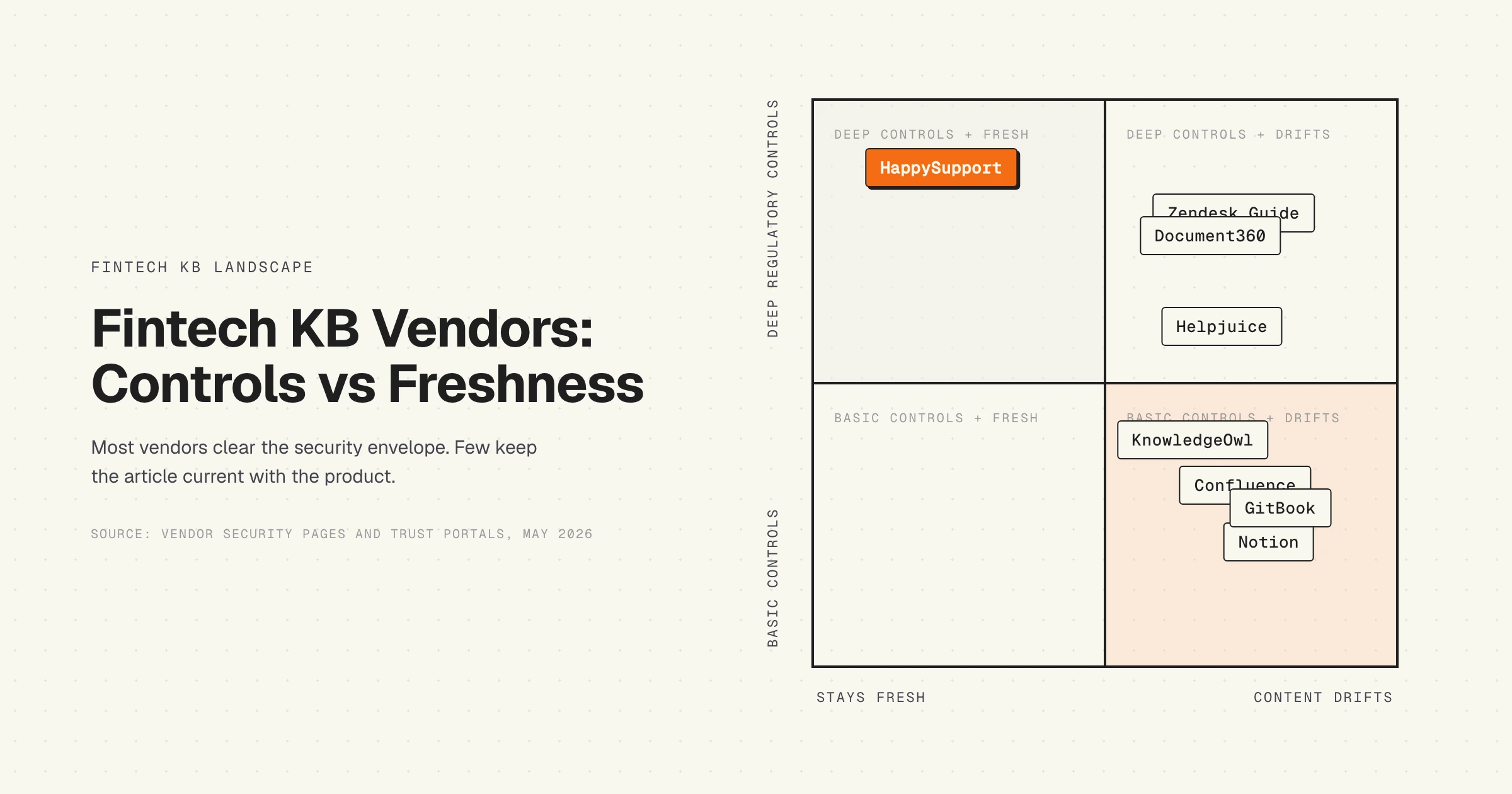

The table below covers four vendors that fintech SaaS teams routinely shortlist. Every claim reflects what the vendor publishes on their security or trust pages, what is reported in independent reviews, or what we have verified directly. Confirm with the vendor before signing because tier requirements, audit log scope, and residency options change.

Three patterns are worth flagging. First, the four established vendors are within striking distance of each other on the security envelope. The differences sit in residency options, log retention, and the specific SOC 2 scope. Document360, Helpjuice, and Zendesk Guide all clear the table-stakes bar. KnowledgeOwl is the one to scrutinize for a regulated fintech because the public attestations are thinner. Second, every vendor that markets a SOC 2 Type II report should provide the unredacted report under NDA. If sales cannot produce it, that is a signal. Third, the accuracy column is where the field divides. Versioning preserves history. It does not flag articles that have drifted out of step with the product. Only HappySupport, by design, surfaces the drift signal as a primary product feature.

What most fintech KB articles skip: the accuracy gap

This is the part of the procurement conversation nobody starts with, and it is the part the regulator notices first.

SOC 2 Type II reports attest to the operating effectiveness of controls. They do not attest that the content inside the system is accurate. The control says "all article changes go through review." The audit confirms the control runs. The audit does not confirm that the published article is current with the product or consistent with the firm's actual practice.

Audit logs prove who changed the article and when. They do not prove the article was right when it was published. Encryption protects the article in transit and at rest. It does not check the article for staleness. Content versioning preserves snapshots of every published version. It does not signal when the snapshot no longer matches the product. The system can be perfectly secure, perfectly auditable, perfectly versioned, and still serving a customer-facing article that says the dispute resolution timeline is 10 business days when the firm's actual practice has moved to 7.

This is not a hypothetical. The pattern shows up in every retrospective from fintechs that have been through a CFPB exam, an OCC review, or a partner-bank audit. The exam team reads the help center. They compare the help center against the policy. They compare the policy against the actual practice. When the three diverge, the exam goes long. We have written about the underlying mechanism in the hidden cost of documentation decay and the freshness-scoring problem that breaks LLM-fronted knowledge bases. The fintech context just turns the cost into a regulatory finding.

Accuracy controls in practice look like this. Every article carries metadata that ties it to the product surface it documents, so when the underlying surface changes the article gets flagged. Articles describing regulated workflows carry an explicit review cadence and a named owner, with automated escalation when the review date lapses. Internal-only articles describing sensitive flows are version-tracked and require sign-off on every meaningful edit. If there is an AI search or AI answer layer, it returns a confidence signal and refuses to answer when the source article exceeds a freshness threshold.

None of this is required by SOC 2. None of it is required by ISO 27001. None of it is required by PCI-DSS. All of it is required by the actual risk model of a fintech SaaS team facing a regulator. The procurement checklist that stops at "SOC 2 Type II yes" misses the point.

A practical 90-day fintech KB implementation plan

Compressed timeline for a fintech SaaS team migrating off Notion, Confluence, or a generic KB to a compliance-ready knowledge base. Built for Seed-to-Series-C teams with a small ops bench and limited compliance specialist time.

Days 1 to 15: scoping and risk analysis

Inventory the existing content. Categorize by regulatory exposure: customer-facing disclosure, internal procedure, agent-only handling note, marketing-adjacent help. Map the inventory to the regulatory frameworks that apply to your firm. Identify which articles describe regulated workflows where staleness is a finding risk. Run the risk analysis with whoever owns compliance, and document the output. This is the artifact the OCR or the partner bank will ask for first.

Days 16 to 40: vendor selection and contracting

Issue an RFP scoped to the eight requirements above. Demand the unredacted SOC 2 Type II report under NDA. Confirm BAA equivalents if any flow may touch HIPAA-adjacent data. Pin the data residency in the contract, not in the marketing page. Verify the tier you are budgeting for actually includes the controls you need. Procurement disasters happen when the BAA or the residency or the SCIM provisioning sits one tier above the plan that got signed.

Days 41 to 65: migration and identity federation

Migrate the content in priority order: regulated workflow articles first, then customer-facing disclosures, then everything else. Federate SSO against your identity provider, set up SCIM for provisioning and deprovisioning, and map role assignments to the existing role model. Verify that the compliance team has read access to every section. Set up the audit log forwarding into your existing log aggregation tool if you have one.

Days 66 to 80: accuracy layer and review workflows

Define review cadences per article category. Assign a named owner per regulated workflow article. Set up automated escalation when the review date lapses. If the platform has drift detection, configure it. If not, build a quarterly review program with a tracked calendar. Document the program because the exam team will ask for it.

Days 81 to 90: dry run

Run the regulator simulation. Pick five articles that describe regulated workflows. Compare each against the actual product behavior, the internal policy, and the most recent product release notes. Document the gaps. Fix the gaps. Run the simulation again with five more articles. By the end of day 90, the KB should be in shape to survive an exam request without scramble.

Common mistakes fintech teams make with their knowledge base

Five failure patterns show up repeatedly when fintech SaaS teams audit their own KB posture. None are exotic. All are avoidable.

The first is treating the SOC 2 logo as the procurement answer. The vendor's marketing page says SOC 2 Type II. The unredacted report says the scope excluded the knowledge base product line, or the report period ended eight months ago, or the report covered the parent company but not the subsidiary that runs the platform. Always read the actual report.

The second is buying the plan without the controls. Procurement signs the Business plan. The audit logs are on Enterprise. The data residency is on Enterprise. The SCIM provisioning is on Enterprise. Months of replanning follow. Always map the requirement to the SKU before signing.

The third is assuming the help center never touches regulated content. It does. A how-to about resetting MFA touches PSD2 SCA. A guide about dispute resolution touches Regulation E and CFPB UDAAP. A guide about closing an account touches GDPR Article 17. The risk analysis should treat every customer-facing article as potentially in scope until evidence says otherwise.

The fourth is forgetting the AI answer layer. If the KB has an AI search or chatbot built on top, the AI vendor sits in the data-processing chain. Confirm the AI provider's SOC 2 posture, confirm there is no training on your data, and confirm the inference pipeline does not log customer data into third-party observability tools you have not vetted. This is the same accuracy-and-trust failure mode we covered in the AI chatbot accuracy gap and in our audit of 30 SaaS help centers for AI readiness.

The fifth is the one regulators see. The KB is compliant, the audit logs are clean, the encryption is documented, and the articles are wrong. Stale fee tables, outdated timelines, references to product behavior that shipped a different way. SOC 2 cannot solve this. The accuracy layer can.

The HappySupport approach for fintech SaaS

HappySupport is built for fintech SaaS teams in the Seed-to-Series-C range that are shipping fast, expecting an exam in the next 12 to 18 months, and tired of the gap between compliant infrastructure and stale content. The platform clears the security envelope: SOC 2 Type II audited controls for access, change management, and encryption; AES-256 at rest, TLS 1.3 in transit; end-to-end audit logs of every edit and every permission change; section-level RBAC federated through your identity provider; EU residency on Enterprise.

What is different is the accuracy layer. HappySupport's recorder captures help center steps as DOM and CSS metadata, not as pixel screenshots. When the underlying product changes, the recorder knows. The article gets flagged for review, the screenshot gets re-captured, and the editor sees the diff. The same pipeline powers a self-updating help center that does not drift away from the product, and gates AI answers on whether the source article is still current.

HappySupport is not the right answer for a tier-1 bank running bespoke procurement and a 200-page vendor security questionnaire. For that segment, the established enterprise vendors with longer-running SOC 2 history and broader compliance attestations are the safer pick. HappySupport is the right answer for a fintech SaaS that needs the security envelope and the accuracy layer in the same product, and needs to ship the result inside a 90-day window.

For teams that have learned what a stale article looks like during a CFPB exam, that gap matters more than another security badge.